Kiyotaki and Moore (1997): Credit Cycles

In their seminal 1997 paper, Kiyotaki and Moore put forth a model of credit cycles in which movements in asset prices interacts with the real side of the economy and produce amplified and persistent effects of shocks to the economy.

Their original model is relatively simple with risk-neutral agents and one-time unanticipated MIT shocks. Peter Frank Paz, a Ph.D. candidate from New York University proposes a more modern extension of the model with risk-averse agents and recurrent aggregate shocks. The model fits squarely in GDSGE framework and Peter kindly contributed his gmod file below.

As in Kiyotaki and Moore (1997) the economy consists of two production sectors, farming and gathering, with population of each sector normalized to one. The farmers are more productive, but are less patient than the gatherers and thus they tend to borrow from the gatherers in equilibrium.

A farmer solves

subject to the budget constraint:

in which her resource is from production

the value of land holding \(q_{t}k_{t-1}\), and bond holding \(b_{t-1}\). The aggregate TFP shock \(A_{t}\) follows a Markov process. She allocates her resource among consumption \(x_{t}\), as well as land and bond holding into the next period. As in Kiyotaki and Moore (1997), here portion \(c\) of the output is non-tradable and has to be consumed, i.e.,

and only the remaining portion \(a\) is tradable. She is also subject to the following collateral constraint:

in which \(\underline{q}_{t+1}\) is the lowest possible land price in the next period. In Kiyotaki and Moore (1997) \(\theta\) is set at \(1\) but we allow \(\theta\) to be smaller than \(1\) in this extension so that the collateral constraint binds with positive probability in the ergodic distribution of the model dynamics.

Similarly, a gatherer solves

subject to the budget constraint,

in which her production function is concave,

We assume the gatherers’ productivity \(\underline{A}_{t}\) is inferior, and equals to a fixed proportion of \(A_{t}\), i.e., \(\underline{A}_{t}=\delta A_{t}\) with \(\delta<1\).

Let us denote the multipliers on the farmers’ budget constraint (17) as \(\beta^{t}\lambda_{t}\), and on the tradability constraint (18) as \(\beta^{t}\eta_{t}\), and on the collateral constraint (19) as \(\beta^{t}\mu_{t}\). Because the farmers and gatherers’ optimization problems are globall concave maximization problems, the following first order conditions and complementary-slackness conditions are neccessary and sufficient for optimality:

The total land supply is fixed at \(\overline{K}\), and the market clearing conditions are

We define recursive equilibrium over two endogenous state variables. The first-one is the farmers’ land-holding \(k_{t-1}\). The second one is the farmers’ financial wealth share defined as

We use \(\left(k_{t-1},\omega_{t}\right)\) as the endogenous state variables, instead of \(\left(k_{t-1},b_{t-1}\right)\) in order to avoid multiple equilibria problems. (The multiple equilibria problem in a similar setting is studied previously in Cao, Luo and Nie (2019).)

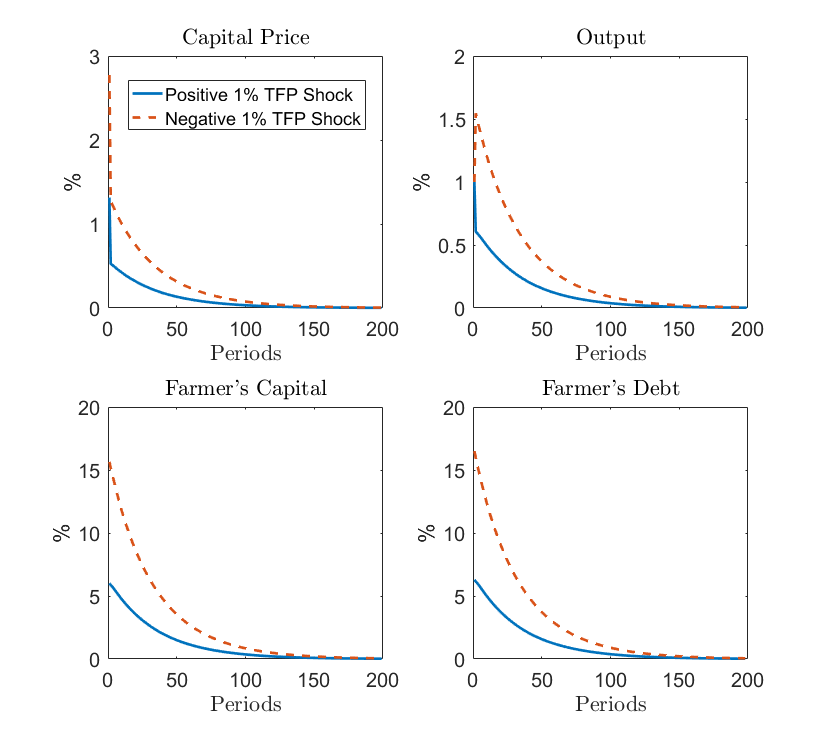

In the numerical exercise, we choose the shock process of TFP \(A_{t}\) to be I.I.D., and \(A_{t}\in\left\{ 0.99,1,1.01\right\}\) with probability \(1/3\) for each possible value. In the ergodic distribution, the probabilities for binding collateral constraint conditional on the three values of \(A_{t}\) are 92%, 80% and 77% respectively. Thus the collateral constraint is more likely to be binding when \(A_{t}\) is low.

The IRFs after positive and negative

1 percent TFP shocks (flipped for negative shocks) are plotted below by averaging the conditional

responses over the ergodic distribution (using the method

from the Guerrieri et al. (2020) example

in the following MATLAB file).

Although the TFP shocks are symmetric and temporary, the IRFs show that their effects are asymmetric and persistent thanks to market incompleteness and the collateral constraint (19). In a more realistically calibrated model, Cao and Nie (2017) study the importance of market incompleteness and collateral constraints in producing these effects. They found that market incompleteness is relatively more important than collateral constraints.

The gmod File

1%========================================================================================

2% PARAMETERS

3%========================================================================================

4parameters a c alower sigma betaF betaG alpha Kbar theta;

5a = 0.7; % tradable productivity of farmer

6c = 0.3; % nontradable productivity of farmer

7alower=0.9; % tradable productivity of gatherer

8

9% preferences

10sigma=1; % risk aversion coefficient

11betaF=0.95; % discount factor of farmer

12betaG=0.98; % discount factor of gatherer

13

14% technology

15alpha=0.7; % coefficient of gatherer's production

16Kbar=1; % fixed capital stock

17

18% credit

19theta=0.9;

20

21SaveFreq = 200;

22PrintFreq = 50;

23INTERP_ORDER = 2;

24EXTRAP_ORDER = 2;

25SIMU_RESOLVE=0;

26SIMU_INTERP=1; % Use interpolation for fast simulate

27IterSaveAll = 0;

28

29%========================================================================================

30% ENDOGENOUS STATES

31%========================================================================================

32var_state kF omega;

33kFPts=41;

34kFMin=0.02;

35kFMax=0.95;

36drift_K = 0.01;

37kF=linspace(kFMin,kFMax,kFPts);

38

39omegaPts=40;

40omegaMin=0;

41omegaMax=0.2;

42omega=linspace(omegaMin,omegaMax,omegaPts);

43

44%========================================================================================

45% SHOCKS

46%========================================================================================

47

48var_shock A;

49

50shock_num=3;

51A = [0.99 1 1.01];

52shock_trans = ones(shock_num,shock_num)/shock_num;

53

54[KMesh,omegaMesh] = ndgrid(kF,omega);

55

56

57%========================================================================================

58% STATE TRANSITION FUNCTION: INTERPOLATION Variables subset of Endogenous variables

59%========================================================================================

60var_policy_init nxF xG eta kFpol R q nbFpol muF;

61inbound_init nxF 0 10;

62inbound_init xG 0 10;

63inbound_init eta 0 1;

64inbound_init kFpol 0 Kbar;

65inbound_init R 0 10;

66inbound_init q 0 10;

67inbound_init nbFpol 0 10; % Transformaion nbFpol = bFpol + theta*q*kFpol

68inbound_init muF 0 1;

69

70var_aux_init loglambdaF loglambdaG logaux;

71

72% This corresponds to the T-1 problem

73model_init;

74 kG = Kbar-kF; % market clearing for capital state

75

76 % Backout bFpol

77 kGpol = Kbar-kFpol; % market clearing for capital policy

78 bFpol = nbFpol;

79 bGpol = -bFpol; % market clearing

80

81 % Backout xG and marginal utility

82 Y = A*(a+c)*kF + alower*A*kG^alpha; % aggregate output

83 xF = nxF + c*A*kF; % consumption of farmer

84

85 lambdaF = xF^(-sigma)/(1-eta); %multiplier for nontradable is eta*lambda

86 lambdaG = xG^(-sigma);

87 loglambdaF = log(lambdaF);

88 loglambdaG = log(lambdaG);

89 aux = (q+A*(a+c)-c*A*eta)*lambdaF;

90 logaux = log(aux);

91

92 % In the last period, people consume everything, and qT=0

93 xF_next = (a+c)*kFpol + bFpol;

94 xG_next = alower*kGpol^alpha + bGpol;

95 lambdaF_next = xF_next^(-sigma);

96 lambdaG_next = xG_next^(-sigma);

97

98 foc_bondG = 1 - R*betaG*lambdaG_next / lambdaG;

99 foc_kG = q - betaG*lambdaG_next*alower*alpha*kGpol^(alpha-1)/lambdaG;

100

101 foc_bondF = 1 - R*betaF*lambdaF_next / lambdaF - muF;

102 foc_kF = q - betaF*(a+c)*lambdaF_next/lambdaF;

103 slack_bF = muF*nbFpol;

104 slack_xF = eta*nxF;

105 budgetF = q*kFpol +bFpol/R + xF - A*(a+c)*kF - omega*q*Kbar;

106 MC_Y = Y - xF - xG;

107

108 equations;

109 foc_bondG;

110 foc_kG;

111 foc_bondF;

112 foc_kF;

113 slack_bF;

114 slack_xF;

115 budgetF;

116 MC_Y;

117 end;

118end;

119

120var_interp loglambdaF_interp loglambdaG_interp logaux_interp q_interp;

121%Time iteration update: update of the transition function after a time iterarion step need to be specified.

122loglambdaF_interp = loglambdaF;

123loglambdaG_interp = loglambdaG;

124logaux_interp = logaux;

125q_interp = q;

126

127initial loglambdaF_interp loglambdaF;

128initial loglambdaG_interp loglambdaG;

129initial logaux_interp logaux;

130initial q_interp q;

131

132%========================================================================================

133% Endogenous variables or policy variables: name, and bounds

134%========================================================================================

135var_policy nxF xG eta kFpol R q nbFpol muF omega_next[3];

136inbound nxF 0 2;

137inbound xG 0 2;

138inbound eta 0 1;

139inbound kFpol 0 Kbar;

140inbound R 0 1.5 adaptive(1.5);

141inbound q 0 10 adaptive(1.5);

142inbound nbFpol 0 10 adaptive(1.5); % Transformaion nbFpol = bFpol + theta*q*kFpol

143inbound muF 0 1;

144inbound omega_next 0 1;

145

146%====================================================

147% Other equilibrium variables

148%====================================================

149var_aux xF loglambdaF loglambdaG logaux bFpol Y bF; %qlow_next

150var_output xF xG Y q R eta muF kFpol omega_next bF;

151

152%====================================================

153% MODEL

154%====================================================

155model;

156kG = Kbar-kF; % market clearing for capital state

157Y = A*(a+c)*kF + alower*A*kG^alpha; % aggregate output

158

159bF = q*omega*Kbar - q*kF;

160

161[loglambdaF_next', loglambdaG_next', logaux_next', q_next']=GDSGE_INTERP_VEC'(kFpol,omega_next');

162lambdaF_next' = exp(loglambdaF_next');

163lambdaG_next' = exp(loglambdaG_next');

164aux_next' = exp(logaux_next');

165

166% Backout bFpol

167kGpol = Kbar-kFpol; % market clearing for capital policy

168quse = GDSGE_MIN{q_next'};

169

170bFpol = nbFpol - theta*quse*kFpol;

171bGpol = -bFpol; % market clearing

172

173% Backout xG and marginal utility

174xF = nxF + c*A*kF; % consumption of farmer

175lambdaF = xF^(-sigma)/(1-eta);

176lambdaG = xG^(-sigma);

177loglambdaF = log(lambdaF);

178loglambdaG = log(lambdaG);

179aux = (q+A*(a+c)-c*A*eta)*lambdaF;

180logaux = log(aux);

181

182mpk_nextplusq'= (alower*A')*alpha*kGpol^(alpha-1)+q_next';

183%Aplusqnext' = A'*(a+c)+q_next';

184

185%====================================================

186% calculate the residual equations: 8 equation (= 7+ 1 consistency) and 8 unknown

187%====================================================

188foc_bondG = 1 - R*(betaG*GDSGE_EXPECT{lambdaG_next'}) / lambdaG;

189foc_kG = q - betaG*GDSGE_EXPECT{lambdaG_next'*mpk_nextplusq'}/lambdaG;

190

191foc_bondF = 1 - R*(betaF*GDSGE_EXPECT{lambdaF_next'}) / lambdaF - muF;

192foc_kF = q - betaF*GDSGE_EXPECT{aux_next'} /lambdaF - theta*quse*muF/R;

193slack_bF = muF*nbFpol;

194slack_xF = eta*nxF;

195budgetF = q*kFpol +bFpol/R + xF - A*(a+c)*kF - omega*q*Kbar;

196MC_Y = Y - xG - xF;

197

198consis_omega_next' = (q_next'*kFpol + bFpol) - q_next'*omega_next'*Kbar;

199

200 equations;

201 foc_bondG;

202 foc_kG;

203 foc_bondF;

204 foc_kF;

205 slack_bF;

206 slack_xF;

207 budgetF;

208 MC_Y;

209 consis_omega_next';

210 end;

211end;

212

213simulate;

214 num_periods = 1000;

215 num_samples = 100;

216 initial kF 0.05;%Kbar - (a/(alower*betaG*alpha))^(1/(alpha-1));

217 initial omega 0.01;

218 initial shock 2;

219

220 var_simu xF xG Y q R eta muF bF; % some variables

221 kF'=kFpol;

222 omega' = omega_next';

223end;